Where Data Tells the Story

© Voronoi 2026. All rights reserved.

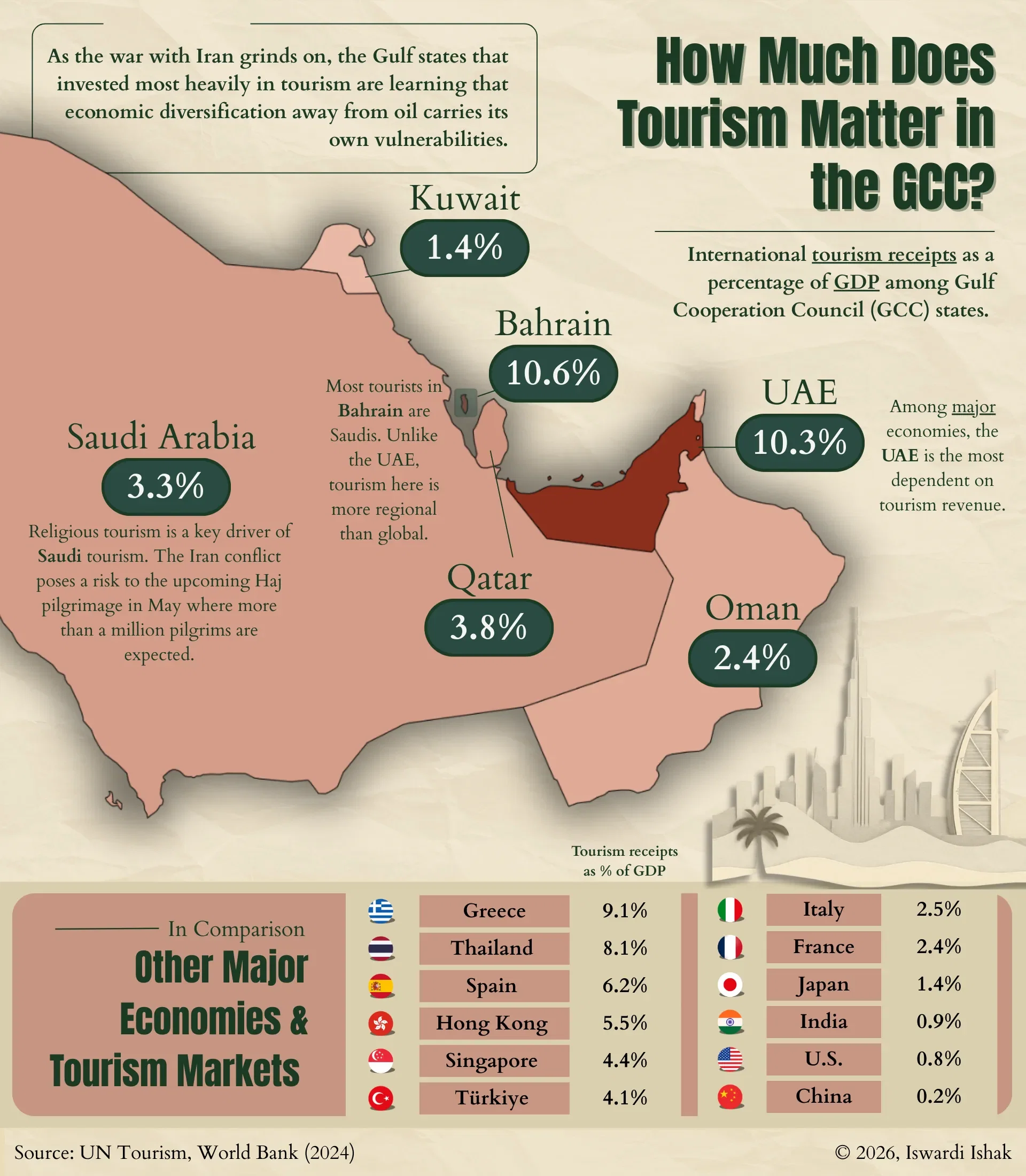

Gulf states discover tourism's double edge

For the Gulf states, diversification away from oil was supposed to reduce economic risk. Tourism, it turns out, comes with risks of its own.

The UAE has built the most exposed position of any major economy, with tourism receipts at 10.3% of GDP ahead of major tourism markets: Greece, Thailand and Spain. Dubai's transformation from desert outpost to global transit hub and leisure destination is one of the more remarkable economic feats of the past three decades. The returns have been substantial. So, now, is the vulnerability.

Bahrain's 10.6% figure is equally striking for a country of its size, though the drivers are different: much of its tourist traffic crosses the King Fahd Causeway from Saudi Arabia for weekend visits, making its receipts less a function of global tourism trends than of its neighbour's domestic mood.

Saudi Arabia, at 3.3%, carries a different kind of concentration risk. Religious tourism, centred on the Haj and Umrah pilgrimages to Mecca and Medina, underpins a large share of tourism revenue. Almost 2 million pilgrims are expected for this year's Haj alone. The ongoing conflict with Iran casts a shadow over attendance, and with it over a revenue stream the Kingdom has been counting on as a pillar of its Vision 2030 diversification strategy.

Kuwait, at 1.4%, and Oman at 2.4%, have yet to make a serious bet on tourism at all. That looks increasingly like a missed opportunity or, depending on how the region's conflicts develop, a prudent hedge.