Where Data Tells the Story

© Voronoi 2026. All rights reserved.

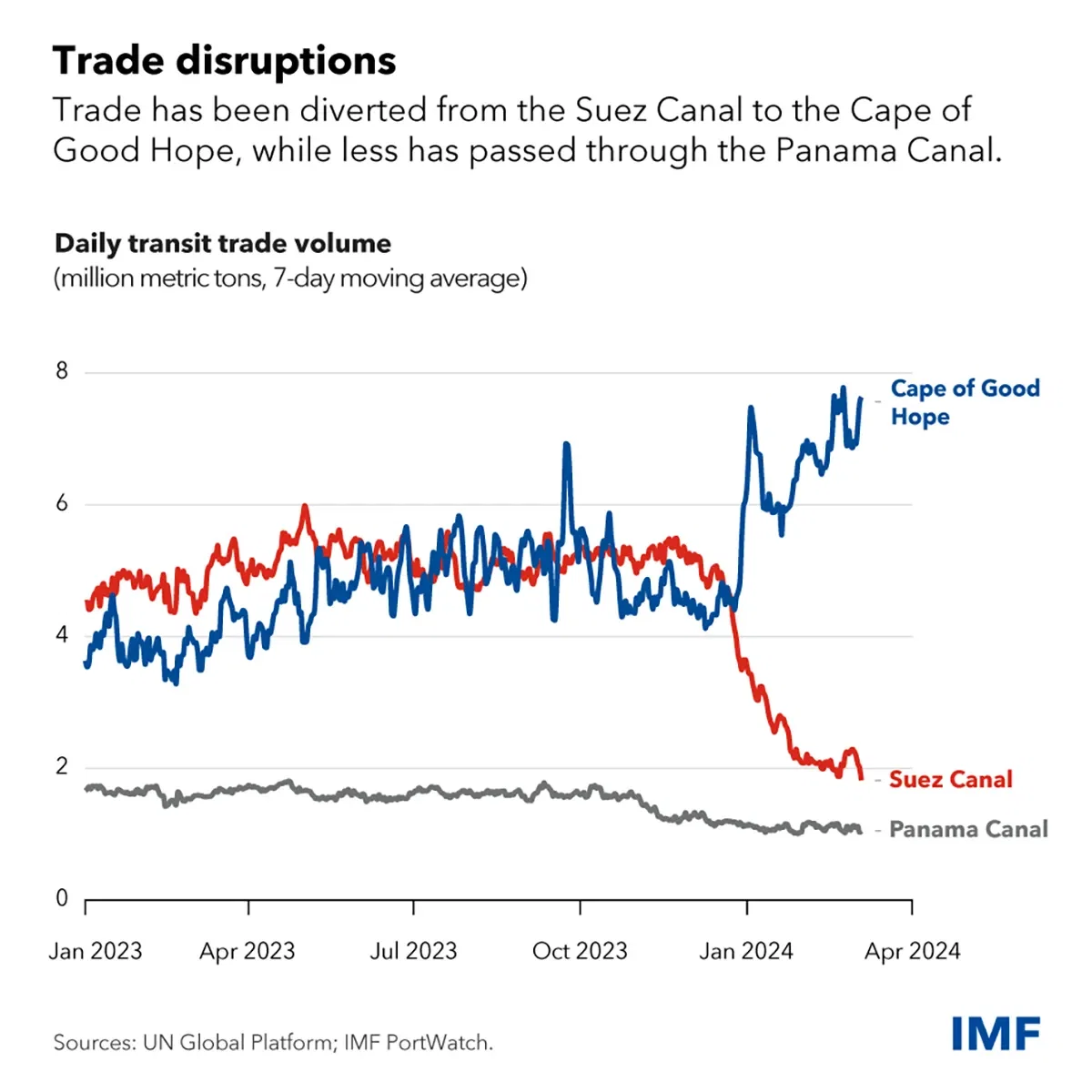

In the past few months, global trade has been held back by disruptions at two critical shipping routes. Attacks on vessels in the Red Sea area reduced traffic through the Suez Canal, the shortest maritime route between Asia and Europe, through which about 15 percent of global maritime trade volume normally passes. Instead, several shipping companies diverted their ships around the Cape of Good Hope. This increased delivery times by 10 days or more on average, hurting companies with limited inventories.

On the other side of the world, a severe drought at the Panama Canal has forced authorities to impose restrictions that have substantially reduced daily ship crossings since last October, slowing down maritime trade through another key chokepoint that usually accounts for about 5 percent of global maritime trade.

This chart uses data from our PortWatch platform to show trade volume that transits through these three critical shipping lanes. Our high-frequency transit estimates indicate that the volume of trade that passed through the Suez Canal dropped by 50 percent year-over-year in the first two months of the year, and the volume of trade transiting around the Cape of Good Hope surged by an estimated 74 percent above last year’s level. Meanwhile, the transit trade volume through the Panama Canal fell by almost 32 percent compared with the prior year.

The platform also shows that in January and February 2024, there was a 6.7 percent decline year-over-year in port calls to the 70 ports we track in sub-Saharan Africa. The corresponding declines for the European Union and the Middle East and Central Asia were 5.3 percent. These decreases likely reflect the transitory effects of longer shipping times. If continued, the ripple effects of these disruptions could temporarily hamper some supply chains in affected countries and cause upward pressure on inflation (in part due to higher shipping costs).

An important implication of these shipping disruptions is that official statistics on recorded imports (and exports) based on customs records may be affected by the temporary impact of ships being re-routed. This will make it more difficult to gauge the underlying momentum of global trade and economic activity in the coming months.

For example, merchandise trade reports for January in many countries in Africa, the Middle East and Europe may show slowing import growth as some imports that would normally have been recorded in January were only delivered in February. For the same reason, many low-income countries that obtain a significant share of their fiscal revenues from import duties (and export taxes) may report lower fiscal revenue than expected for January.