Where Data Tells the Story

© Voronoi 2026. All rights reserved.

In her March 2026 Spring Statement, Chancellor Rachel Reeves announced no new major tax hikes or significant spending plans, maintaining her commitment to a single annual fiscal event.

The previous Autumn 2025 Budget was a different affair - one of significant tax raises. Here, the Chancellor announced the freezing of Income Tax and National Insurance Contributions thresholds until 2031, creating what is known as “fiscal drag” (wages increase but tax thresholds don’t change, leading to more people being dragged into higher tax bands) and the highest tax burden in 70 years.

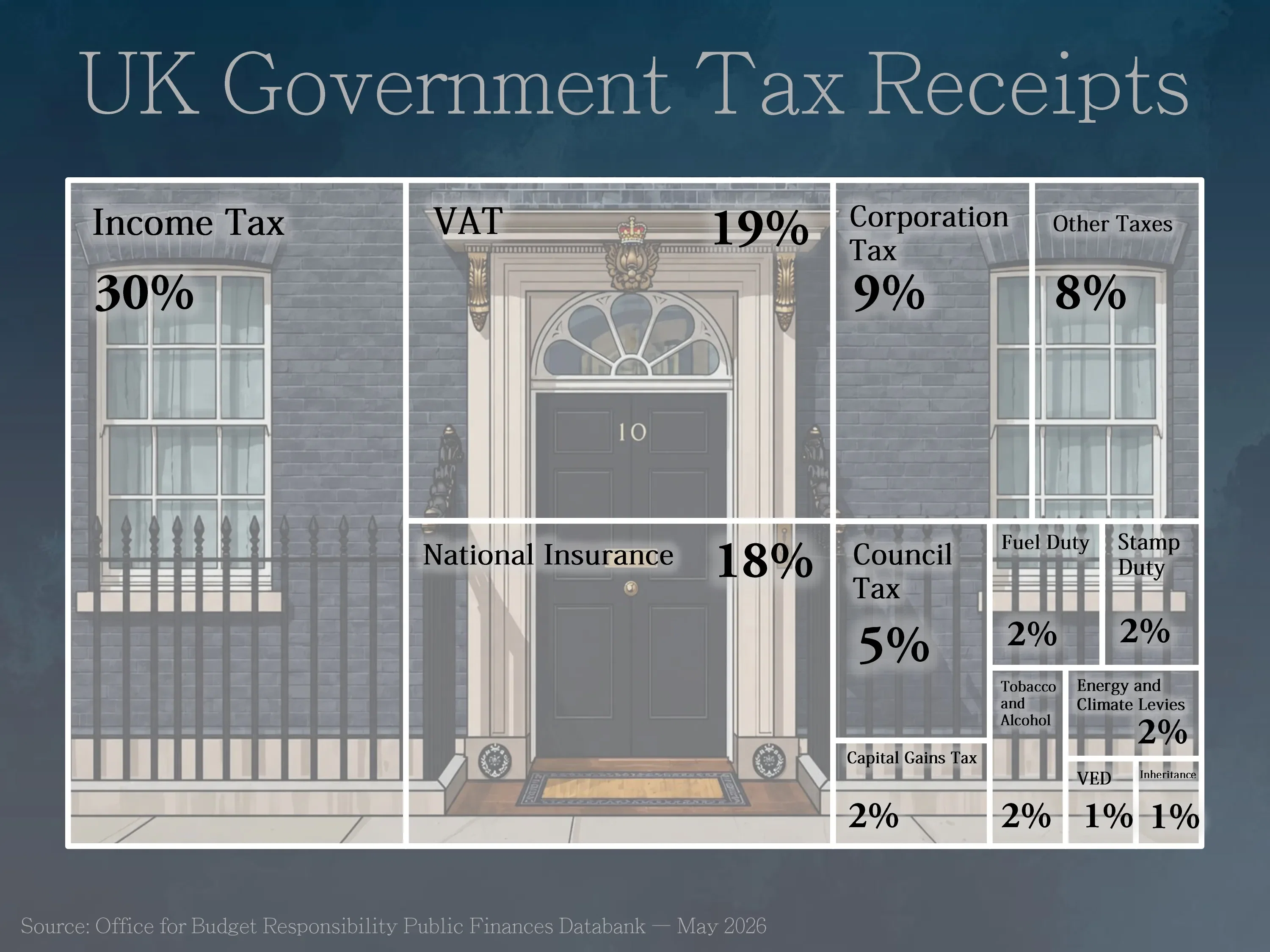

The dataset tells a remarkably clear story of government tax receipts being heavily anchored on labor and consumption. Out of a projected total revenue of £1,108 billion, just three tax streams account for more than two-thirds of all receipts.

This distribution highlights a fundamental economic reality: the fiscal health of the state is directly tethered to individual employment and consumer confidence. Because Income Tax and National Insurance both tax payrolls, a staggering 48% of total government revenues relies strictly on employment levels and wage growth.

The freezing of personal tax thresholds from April 2028 to April 2031 is projected by the Office for Budget Responsibility to raise over £23 billion in total by 2030/31.

Corporate receipts are crucial but volatile

Further down the ledger sits Corporation Tax, providing 9% of total receipts.

While 9% may seem modest, it represents the single largest pool of revenue extracted directly from commercial entities. From an analytical standpoint, corporate tax revenues are notoriously cyclical. While employment and basic consumption (like food and utilities taxed under VAT structures) remain relatively stable even during market downturns, corporate profits fluctuate with global economic cycles.

The long tail of smaller taxes

The remaining smaller categories might seem insignificant. For instance, Inheritance Tax and Vehicle Excise Duty combined make up just 2% of the total budget. However, decision-makers view this long tail through a completely different lens: incentive structures.

Many of these smaller line items are not designed solely to raise capital - they are behavioral instruments. Fuel duties, Vehicle Excise Duty, and Energy and Climate levies (combining for £51 billion) double as environmental policy tools meant to price carbon emissions and fund green infrastructure transitions. Similarly, taxes on Tobacco and Alcohol act as corrective mechanisms to offset public healthcare costs.

For corporate strategists and long-term planners, the takeaways are clear:

The impact on debt to GDP

Government debt was equivalent to 93.6% of GDP at the end of 2024/25. The OBR forecasts that it will increase to 97.0% at the end of 2028/29. It will then fall to around 96.1% of GDP at the end of 2030/31.

Ultimately, the data shows an ecosystem designed to absorb localised shocks by anchoring itself firmly to the broader, more predictable rhythms of the national workforce.