Where Data Tells the Story

© Voronoi 2026. All rights reserved.

As 2024 starts, the good news is that there haven’t been any notable requests by a low-income country for comprehensive debt relief since Ghana’s, more than a year ago. Despite this, vulnerabilities remain, with high debt servicing costs a growing challenge for low-income countries.

Financing pressures due to relatively high interest payments and the pace at which low-income countries need to repay debt are straining budgets. That prevents these countries from spending more on essential services or the critical investment needed to attract business, create jobs, improve prosperity, and build climate resilience.

One important metric is the share of revenues the government collects from its population through taxes and other fees that goes to pay its foreign creditors. While the scale of the burden differs greatly across countries, it’s generally about two and a half times higher than a decade earlier. This means for a typical low-income borrower the share has risen to about 14 percent, from about 6 percent, and as much as 25 percent, from about 9 percent in some economies. This is one of the key indicators used in the framework for assessing debt sustainability that signals a country might be at risk of needing financial support from the IMF or of missing a debt payment.

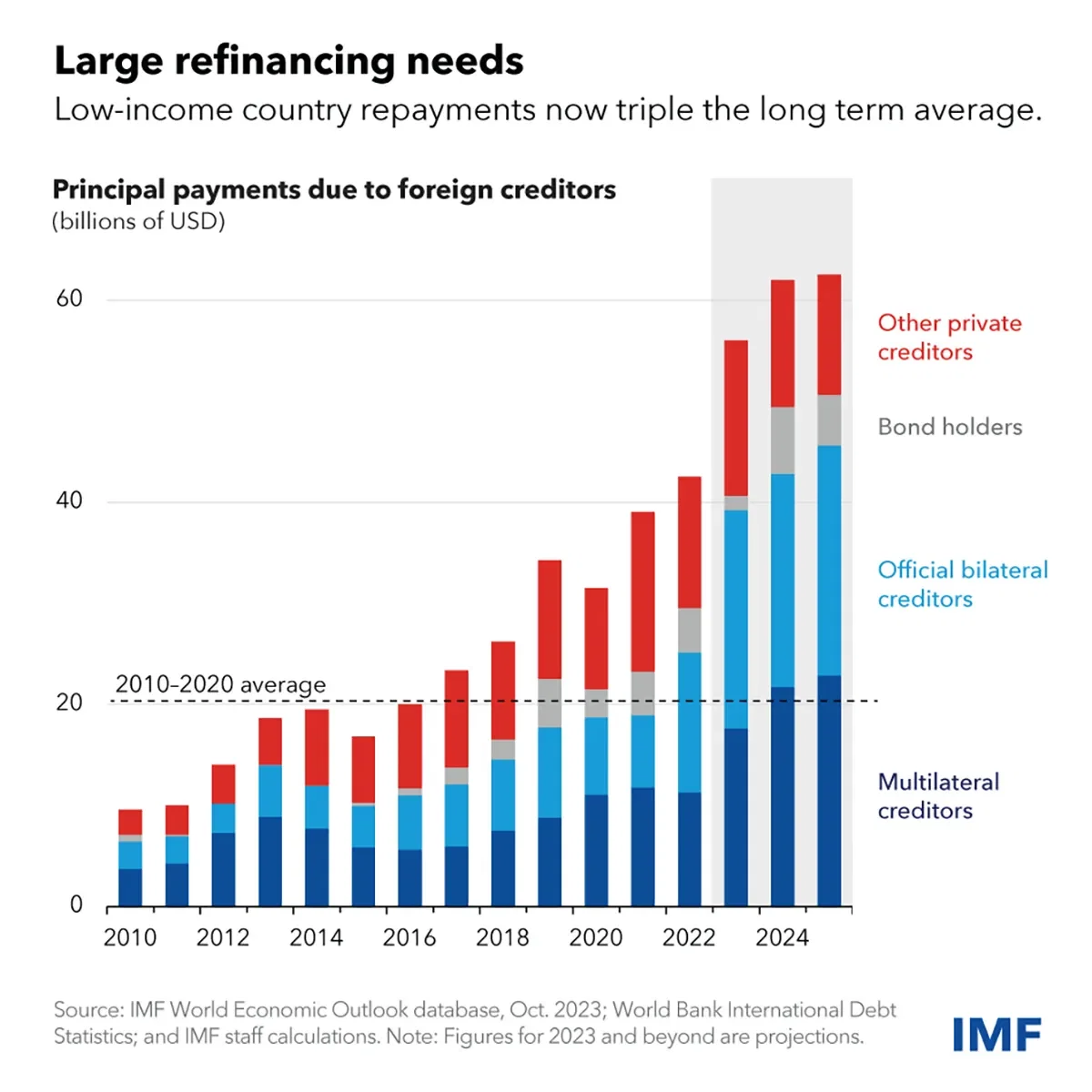

Low-income countries also have significant debt repayments falling due in the next two years. They need to refinance about $60 billion of external debt each year, about three times the average in the decade through 2020. But with many competing demands for financing, including from advanced and emerging market economies that are also trying to adapt to climate change, there’s a significant risk of a liquidity crunch—failure to raise sufficient financing at an affordable cost. That could in turn lead to a destabilizing debt crisis.

To address this financing challenge, we must understand why it’s happening and what affected countries and the broader international community can do to help.

See the full article here.