Where Data Tells the Story

© Voronoi 2026. All rights reserved.

On Sunday, Claudia Sheinbaum made history.

With just shy of 60% of the total vote, the 61-year old former head of Mexico City became the first woman ever elected president in Mexico. She will take office on the 1st of October, replacing her political ally and outgoing president Andrés Manuel López Obrador.

Sheinbaum will enter office with the support of the over 33M people who voted for her and the backing of López Obrador’s hegemonic MORENA party. But she’ll have lots of challenges facing her.

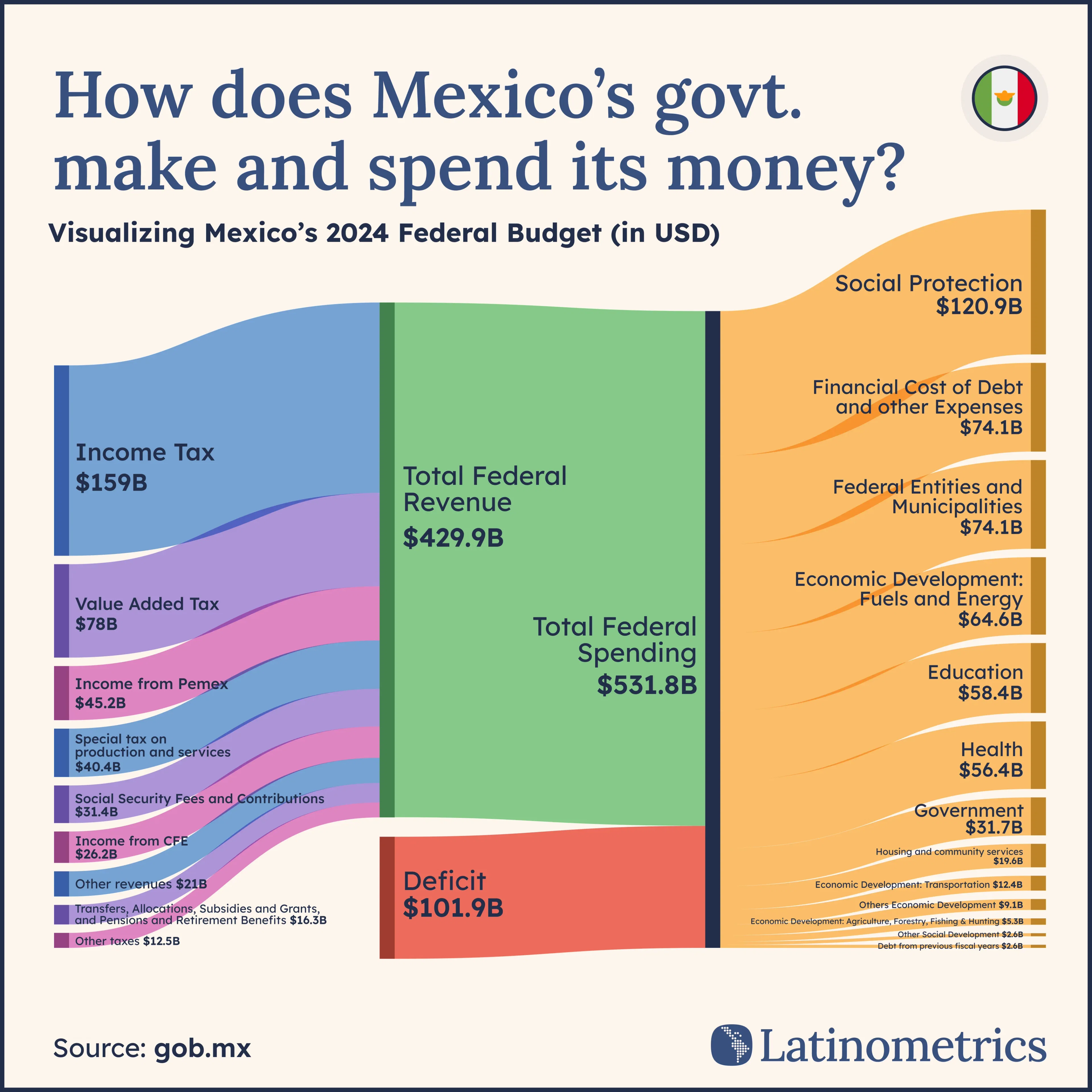

One big one is tackling Mexico’s fiscal deficit, which has steadily climbed leading up to this year’s massive general election. The country is over $100B in the red, a deficit reflcting more than 5% of total GDP. This figure is the highest it’s been in over three decades.

In fact, Fitch Ratings expects overall government debt to reach 48.8% this year, up from last year’s 45.6%. Substantial public investments by the López Obrador administration into massive infrastructure projects, particularly in the counry’s south, has helped accelerate this rise in debt.

However, many of the larger slices of the pie – from pension increases to social programs to assistance to state-owned oil firm Pemex – will be harder to reverse as the Sheinbaum administration seeks to tackle the country’s debt. And the last of these, involving dealing with a notoriously mismanaged and unstable nationalized firm, will be especially difficult.

Expected supermajorities for MORENA in both houses of Congress mean that Sheinbaum will have a strong hand in trying to pass her party’s policy priorities—even if they also spooked investors and contributed to the stock market losing roughly 5% of value by Monday morning.

In any case, President-Elect Sheinbaum and her MORENA allies have lots of work to do. One priority will certainly need to be reining in the deficit while keeping an eye on the country’s most vulnerable populations.