Where Data Tells the Story

© Voronoi 2026. All rights reserved.

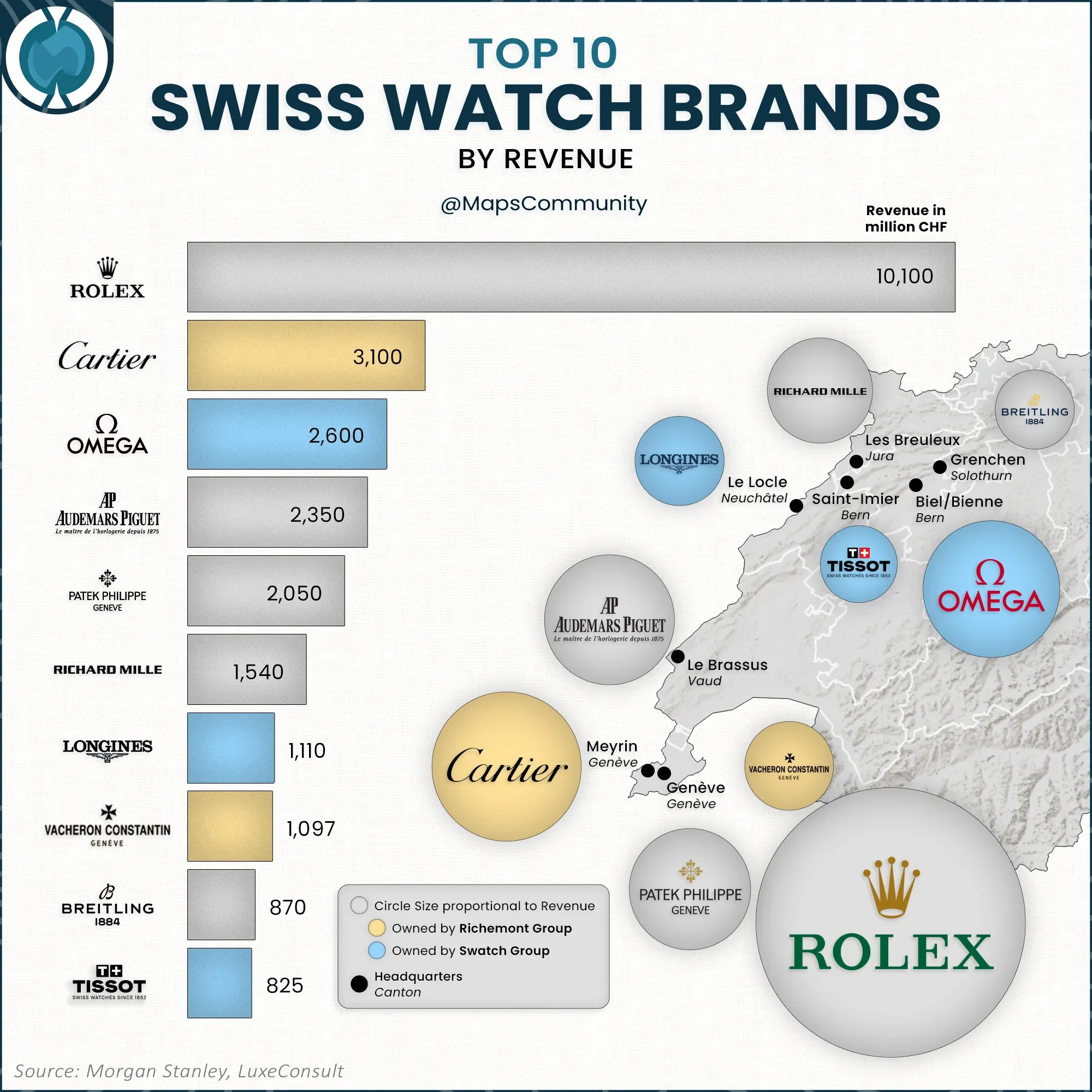

An analysis of the top-tier Swiss watch market reveals a staggering degree of financial and geographic consolidation. A single entity, Rolex, commands an outsized market share, generating 10.1 billion CHF; a figure that precisely equals the combined revenue of its four closest competitors: Cartier, Omega, Audemars Piguet, and Patek Philippe. Furthermore, the industry operates on a distinct geospatial duality. The Canton of Geneva serves as the financial epicenter for ultra-luxury, housing Rolex, Cartier, Patek Philippe and Vacheron Constantin. This localized cluster alone captures nearly 64% of the top ten's total revenue, representing over 16 billion CHF concentrated within a microscopic geographic footprint.

Conversely, the manufacturing hubs stretching across the Jura mountains and Bern cantons act as the engine for conglomerate-backed volume and mid-tier luxury. The Swatch Group (Omega, Longines, Tissot) strategically dominates this northern corridor, capturing roughly 17.7% of the top ten revenue pool. This spatial division highlights a bifurcated supply chain strategy: Geneva acts as the heritage and status center for independent giants and Richemont, while the northern valleys sustain the industrial scale of the Swatch conglomerate.